UK offshore wind - where next?

The latest auction results raise some big questions about where the industry goes now

By Jonny Marshall

Share

Last updated:

The UK’s September 2019 renewables auction delivered – yet again – results that have taken the energy sector’s breath away. Projects penning deals at less than £40/MWh, costs unrivalled by anything else being built today, have drilled the final nail into the coffin on the arguments around high costs of low carbon power.

And in doing so, it has opened up a whole new set of questions that could determine how the sector moves on from here.

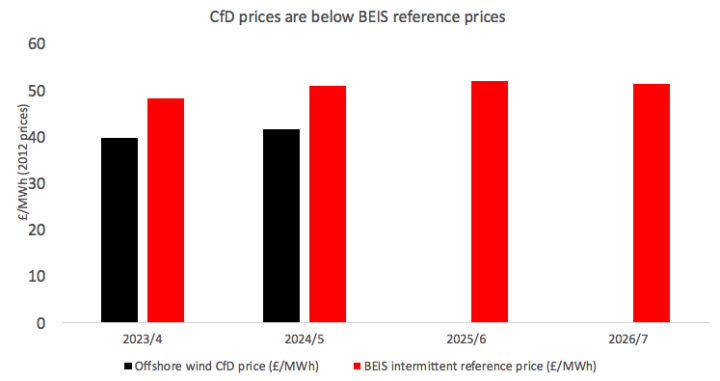

Payback time

As the debate changes away from how much clean power is going to cost, the latest wave of renewables have drawn a clear line in the sand. With projects for delivery in 2023/24 clearing at £39.65/MWh (all prices are in £2012 for continuity with official documents) and those for 2024/25 at £41.61/MWh – a weighted average of £40.67/MWh – all projects are well below where BEIS sees wholesale prices in the middle of the next decade.

In fact, the intermittent reference price (the forecast wholesale price expected when variable renewables are feeding into the grid) for this auction averages £50.54/MWh over the four years detailed in BEIS documents; nearly a tenner per megawatt hour more.

This ~6GW of renewable capacity will generate close to 28 TWh per year, thereby ‘paying back’ a notional £246 million per year, once all up and running. Not bad for something that was considered a blight on British billpayers until very recently.

Hands on

Another effect of the rock bottom prices is that the pot of cash allocated for this auction was not exhausted. The limiting factor, instead, was the capacity cap put into place by the government.

If this situation remains the same going forward – and it is hard to imagine a jump in costs that mean it won’t – it changes the role of the government in the offshore wind revolution.

Rather than limiting rollout rate by spending, it will now be controlled by how much new capacity the government wants to see in each auction. This is a far more hands-on role than the government has historically taken, and effectively puts it in charge of the relative make-up of the UK’s electricity mix in decades to come. Combine these events with a fresh energy minister, and we are in very new territory.

Industry and NGOs have been lobbying for the cap to be raised – perhaps in anticipation of such low prices – calls which will surely become louder as all of the UK’s energy eggs remain in the offshore wind basket, which now falls fully under government control.

Can onshore wind stand up?

Pressure to provide a route to market for offshore wind has focussed on bill savings – with recent analysis for RenewableUK showing that a sizeable onshore wind rollout could shave £50 from bills.

But now, with offshore wind delivering such breathtaking costs, its onshore cousins have their work cut out.

Higher wind speeds at sea, scaling up projects to 1GW+ and an industry that has been supported for years could see offshore wind outcompete land-based alternatives.

And with modelling of Pot 1 auctions showing clearing prices of around £45/MWh, this is one possible reality. It could even see even more focus on offshore wind and a total shunning of onshore wind that isn’t planted on remote islands.

With the Government seemingly reluctant to move on onshore – despite a litany of polls showing its popularity, the potential for community benefit funds and the need to repower ageing turbines – low offshore prices could potentially herald a downturn in onshore prospects.

One exception, however, is September’s remote island wind results. The first onshore schemes to receive government backing in years are based on the latest onshore technology and suffer from high transmission costs – if companies can build them on islands miles from shore at the £40/MWh marker, it should be possible for even less on the mainland.

Only way to know for sure, hold an auction in which all low carbon technologies can compete.

Share