Carbon pricing and CBAMs; what, why, how?

The theory, history and options for carbon pricing.

By Jess Ralston

@jessralston2Share

Last updated:

What is a carbon price?

A carbon price is a charge on carbon emissions, usually levied on the carbon content of goods or services. By applying a cost that increases over time, carbon prices incentivise cleaner means of producing things, or reduce demand for high carbon goods and services by increasing prices.

The aim of a carbon price is to drive carbon emissions reductions by ensuring that polluters pay for their emissions. Carbon prices can be applied economy-wide or targeted towards specific sectors, as is currently the case for the power sector in the UK.

Carbon pricing in some form has been implemented in over 40 countries to date, including the EU, New Zealand, India, Mexico and China. Overall, it is thought that about 25% of global greenhouse gas emissions were covered by carbon pricing schemes in 2021, which rose from 18% in 2020 after China expanded its carbon pricing scheme.

In the UK, an emissions trading scheme has been present since 2002, which widened to the EU emissions trading scheme in 2005. The EU ETS covers manufacturing, aviation and power. These sectors also take part in the UK Emissions Trading Scheme after Brexit, and the power sector in the UK has been subjected to an additional carbon price since 2013.

The positives and negatives of carbon pricing have been discussed for decades, with the Climate Change Committee recently referring to them as ‘an important part of the policy toolkit’ as they can ‘support the public finances while strengthening incentives to reduce emissions’ on the pathway to net zero.

Pricing carbon: taxes or trading

Carbon taxes

Carbon prices can be levied through fixed rate taxes on goods and services. This is known as a ‘carbon tax’ and includes taxes such as the Carbon Price Support (CPS) in the UK.

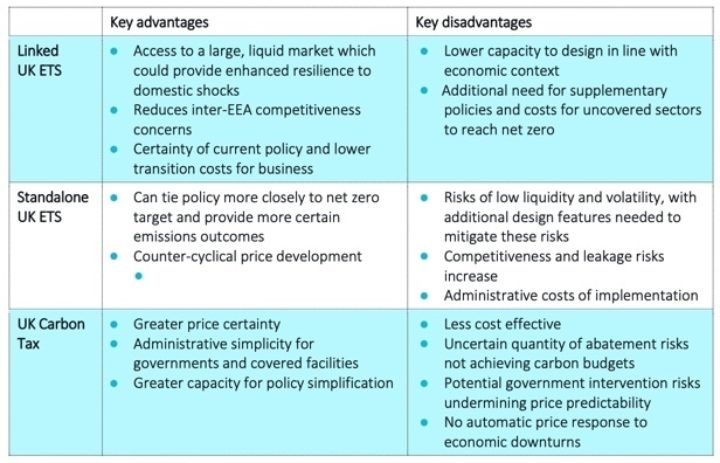

Proponents of a carbon tax say that it is a simple method of reducing emissions by applying a cost to carbon as it provides greater price certainty and administrative simplicity. Carbon taxes can be tailored to suit different sectors, with different prices, and can (in theory) provide longer term clarity on carbon costs than a market driven carbon price.

However, opponents argue that it is difficult to set and maintain a price at a level to drive decarbonisation cost-effectively. For a tax to be effective it needs to be set at an impactful level, with a set trajectory in the future. This also means it can be rendered ineffective during financial downturns.

The inability for governments to decide policies in perpetuity also adds uncertainty. Carbon taxes can be amended or removed quickly, and therefore do not provide investors with the same levels of confidence in comparison to other governmental measures.

Carbon trading

Carbon trading does not set a fixed price for carbon, instead it lets the market decide how much emitting carbon should cost. By issuing a limited number of permits for emissions, the number of which is reduced over time, trading schemes aim to avoid the inherent uncertainty associated with a Government-controlled carbon tax.

One example of carbon trading is the EU ETS. Here, carbon emissions can be bought and sold via auctions, in which allowances are procured to cover emissions from power stations, industry and other sectors. If a company invests in cleaner production processes, it will procure fewer allowances.

Trading schemes also need to balance certainty and flexibility, ensuring that market downturns do not render them ineffective, as was the case for the EU ETS in the years after the 2008 crash. Years of negotiations resulted in the formation of a ‘stability reserve’ that would mop up surplus credits, supporting prices to a level at which they became effective.

In Autumn 2020, EU ETS permit prices started to rise sharply, reaching over €80 per tonne of carbon in December 2021. In the UK-only ETS, after Brexit, carbon prices started at £47 per tonne but, like the EU ETS, rose to around £75 per tonne in late 2021.

The prices of permits in both the EU and UK ETS have levelled out in 2022 and 2023, but still see significant peaks and troughs. The EU ETS price has remained slightly higher than in the UK.

In time, the UK ETS could be linked to the EU system, which could provide access to a larger market with increased liquidity. Larger markets also limit volatility, giving more certainty to market participants. A linked ETS could also reduce competitiveness between organisations in the European Economic Area, as the carbon prices would be the same in the UK and in the EU, and an increased certainty about the policies in place could lower costs for businesses.

However, a UK-only ETS has advantages too, including being able to tie the ETS more closely to the UK’s net zero policy and counteract any slumps or sharp rises in the carbon price, by Government intervention. This is known as counter-cyclical policy.

Carbon Border Adjustment Mechanisms (CBAMs)

For both carbon taxes and trading systems, carbon border adjustment mechanisms (CBAMs) can be applied to prevent imports – not subject to the same level of carbon pricing – from undercutting domestic goods and services. This is known as carbon leakage.

CBAMs work by applying the same domestic carbon price to imported goods and services, to ensure that domestic trade is not placed at a disadvantage. The EU has voted to introduce a CBAM from 2026 and the UK Government has confirmed that it will consult on bringing one in too. This could allow the EU and UK ETS to be linked more closely, as discussed above.

However, CBAMs are highly complex and complicated, in theory accounting for the total supply chain emissions of all imports. They bring significant logistical burden, and have been described as undesirable by leading figures, including US climate envoy John Kerry. CBAMs would also involve the removal of free allowances - given to industries to prevent them moving abroad to avoid paying a carbon price - which could be complicated or politically complex.

Proponents, however, point to CBAMs as a way of using carbon pricing as a tool to cut carbon and preventing cheaper and dirtier products from overseas undercutting domestic industries.

Political considerations

Essentially, carbon prices are a means of implementing the ‘polluter pays’ principle, internalising the cost of carbon. Depending on the elasticity of different parts of the economy, they can either be used to raise revenue or to cut carbon.

Raising carbon prices on petrol, an inelastic product, would raise tax take. It would also lead to undesirable consequences – higher costs of living, for example – as an immediate substitute is not available.

Demand for domestic air travel, on the other hand, responds rapidly to price; it is an elastic product. The ready availability of train or road transport means increases in the cost of internal-UK air tickets will see demand fall.

Politicians will look to balance these two factors in implementing new carbon prices. The issue of ‘lost revenue’ for Treasury as cars, vans and lorries use less petrol and diesel has been highlighted as an issue. In theory, all carbon taxes should ultimately lead to changes in behaviour that sees the amount of revenue they raise fall to zero.

Some commentators have questioned whether carbon taxes could be regressive but it is unknown how much of the carbon tax on businesses is absorbed by the organisation and so also unknown whether it impacts the consumer to any significant degree.

Carbon pricing around the world

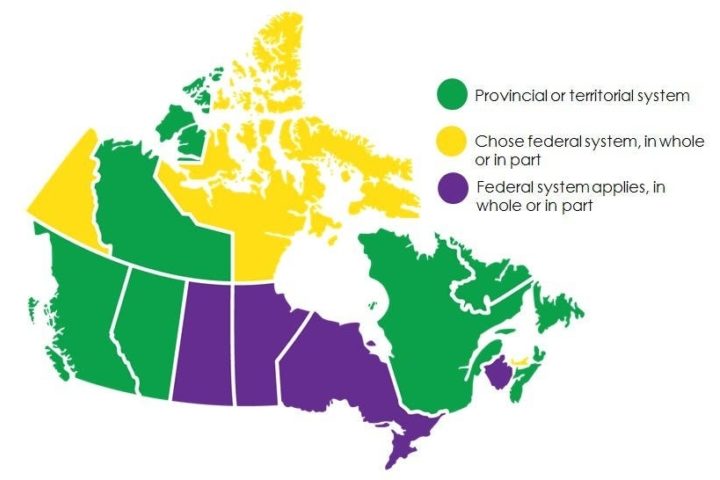

In Canada, a carbon tax scheme is applied to both industries that emit carbon, at $30 per tonne of carbon in 2020 (rising to $50 per tonne in 2023), and consumers. The price paid for carbon per household depends on the area, for example ranging from $439 in Ontario to $720 in Saskatchewan. However, the money collected from households is given back to them through tax returns and the majority (70%) actually receive more back than they paid for carbon. This increases the acceptability of the scheme to households however it is still not universally popular – the premier in Ontario has previously described it as ‘the worst tax ever’.

Similarly, in Australia carbon tax has been a politically divisive issue. In 2012 a carbon tax was introduced at around €15 per tonne of carbon but repealed just two years later when an opposition party won the election. The party campaigned on an ‘axe the tax’ message as, among other issues with the scheme, it was thought the tax increased electricity costs by around 10%.

Future of carbon pricing in the UK

The UK ETS will be reviewed in the context of introducing a CBAM, likely at some point in 2023, with trading continuing in auctions. A flat carbon price on consumers (including sectors such as food) has been ruled out in the near-term, although this is likely to be an ongoing discussion for reaching net zero by 2050.