UK sitting out global clean tech race

As the US and the EU compete to invest in clean tech deployment, does the UK risk being stuck in the middle by its decision to delay its green industrial strategy until the autumn?

By Gareth Redmond-King

@gredmond76Share

Last updated:

Subsidies to the left of us, regulatory freedoms to the right; here we are - stuck in the middle with policy uncertainty and limited investment. That is where the UK government's ‘green day' risks leaving us, having passed without new measures specifically aimed at responding to the intensifying clean tech deployment race between two of the world's biggest economies.

Inflation Reduction Act

In summer 2022, the United States Congress passed a remarkable piece of legislation with unprecedented funding for tackling climate change: the Inflation Reduction Act, or IRA. As the planet's biggest emitter of greenhouse gases, and proud owner of its largest economy, America has finally put serious money where its mouth is on climate change.

$369bn of serious money, in a mix of direct funding and tax credits, to drive development and deployment of clean tech to speed US decarbonisation. It came hard on the heels of a couple of other acts with major funding attached: $54bn via the CHIPS and Science Act for solar and battery development, and $98bn from the Infrastructure, Investment and Jobs Act. Totalling more than $500bn, this triples annual US spending on climate. And, leveraging other federal and state funds, as well as private investment, some analysts put the likely value of the package at around $1.7tr.

The IRA has been controversial beyond US borders however, because of measures designed to support manufacturing within those borders. Politicians from the EU, UK and other major economies have decried it as ‘protectionism'. Despite analysis showing that direct fiscal support to US-based clean tech manufacture accounts for only seven to 11 per cent of the IRA total, it has provoked a remarkable response from the EU.

Europe's response

In March, European Ministers adopted regulatory and policy measures to counter the threat they believe IRA poses in luring European clean tech companies across the Atlantic. Rather than simply set out to match IRA's funding total, the EU has turned to regulatory and policy reforms.

These include speeding up and simplifying planning, enhancing skills needed by the clean tech sector, and relaxing rules on financial benefits that member states can offer to companies - known as state aid. They also agreed measures to diversify source-countries for critical materials - including the metals and rare earths used in batteries - and to increase the proportions sourced and processed within the EU.

The EU's moves recognise the scale of net zero to the European economy - 4.5 million green jobs in 2019, quite some time before the bloc sped up its transition to clean, renewable energy as a means of ending reliance on Russian oil and gas in the wake of Putin's invasion of Ukraine. As an international leader in climate action in recent decades, the net zero economy is also hugely important to the UK. Recent analysis from ECIU and CBI Economics suggests it adds over £70bn a year in value to the economy, employing 840,000 people - some four to five times the number of jobs in the oil and gas sector.

That value and those jobs, not to mention further growth of the sector, risk being threatened if clean tech businesses look to the US or the EU for future growth opportunities. Which is what energy sector trade bodies argue will happen if the UK government doesn't act to make the policy and regulatory environment in the UK more attractive - changes like lifting the continued de-facto ban on onshore wind in England, for example.

Putting the funding to work

It is not as if the US is taking its time in getting the IRA value out of the door. Analysis suggests that the six months since IRA was passed saw over 100,000 new clean energy jobs created in 31 states, representing nearly $90bn in new investment. The same analysis suggests IRA will deliver nine million new green sector jobs over the next decade.

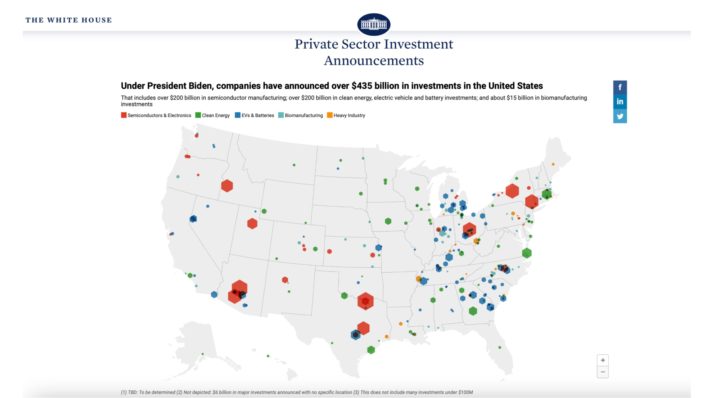

But this didn't just start with IRA - the White House claims US companies have committed $200bn of new clean energy investment since Biden's election.

Policy signals sent by the IRA are just part of the wider political capital invested in climate action by Joe Biden, cemented in the US' more ambitious Paris Agreement targets. And we continue to see this post-IRA, with Biden expected to set tougher automobile pollution levels to drive electric vehicle uptake even faster than existing targets.

Mid-term elections in 2022 also suggested that a new confidence amongst Democrat candidates to put climate front and centre in their campaigns stemmed a feared haemorrhaging of seats to their climate-denying opponents. And it is clear the clean sectors fuelled by IRA are increasingly important in Republican political strongholds, and in areas which feel economically left-behind - something only underlined by specific spending announcements targeted to poorer, ex-mining communities, for example.

Policy signals

All of this adds up to more than just a very big sum of cash and tax credits - a policy environment that gives investors certainty about the relative risks of putting their money in clean energy, rather than fossil fuels.

That policy environment is already paying dividends for the US. Recently, Volkswagen announced that a planned new electric battery plant would be sited in Canada, rather than in Europe, to service the expected growth in the North American market that IRA will drive. Although BMW recently confirmed their commitment to the UK, the motor manufacturers' trade body, and other car industry experts, warn that the UK's car sector could disappear without a response to US and EU moves, as UK electric van start-up Arrival indicated its possible departure for American shores. Not just car firms; companies in energy intensive sectors, like packaging, have recently issued similar warnings about the deterrent effect of a lack of policy clarity.

UK sitting on the sidelines

All of which leaves many observers puzzled as to the delay in a UK response. Shortly before the government's March ‘green day', Chancellor Jeremy Hunt said a UK green industrial plan would be delayed until autumn.

Meanwhile, Labour plans to commit not just to regulatory reform, but to £28bn a year in green spend over eight years - totalling £224bn. For an economy eight times smaller than the US, that would see the UK committing to nearly half the overall recent US commitment, and 60 per cent of the IRA total.

What ‘green day' did confirm, however, was that current policies are not enough to put the UK on track to meet its carbon budget. Meaning that, not only are the UK's growing net zero economy and its reputation as a global climate leader on the line, but so too is progress to deliver our legally binding targets to decarbonise. This despite the UK's track record with clever, and trailblazing, financial incentives to leverage huge private funding to deploy renewables; measures that saw the UK become a leader in offshore wind.

All in all, particularly if more companies begin to eye moves to US and European markets, autumn looks oddly and dangerously far away for a British response to prevent the UK from being squeezed out.

This piece first appeared in Business Green on 17th April, 2023

Share