Low carbon heat abroad

What are other countries doing on het decarbonisation?

By Jess Ralston

@jessralston2Share

Last updated:

To meet increasingly stringent climate targets, countries are now looking to cleaner sources of heat. The European Commission has identified that 50% of the EU’s annual energy consumption comes from heating and cooling – mostly generated by fossil fuel gas.

However, the strategic vision set out in 2018 for a climate neutral Europe expects natural gas to fall to around 5% of total energy consumption in 2050.

On a national level, Sweden, France, Denmark, New Zealand and Hungary all have a net zero emissions target in place for 2050. To meet these goals, emissions from buildings will need to be eliminated.

Sweden has set a target to completely phase out fossil fuels use in heating by 2020 which is progressing well - in 2017, around 75% of energy for heating buildings came from low carbon sources. Similarly, Denmark and France aim to increase their share of renewable heating in line with climate change targets, with Denmark aiming to meet all heat demand with renewables by 2035 and France aiming for 33% by 2020. In 2017, France achieved 21% of heating and cooling from renewables, so it has some way to go to reach the 2020 target.

However, circumstances differ depending on the country. In New Zealand, for example, families tend to heat only their living areas rather than the whole house, and air source heat pumps are found in over a fifth or homes. In fact, sales of air source heat pumps more than tripled between 2003/4 and 2008/9, despite no significant Government policy to support them. In Sweden, there is a greater reliance on district heating from a biomass source for densely populated areas and heat pumps for those more isolated properties.

Minimising energy demand with efficiency measures

The UK’s housing stock has a poor energy efficiency compared to many European neighbours – it was ranked worst out of 16 countries when analysed for fuel poverty, and homes in the UK lose three times more heat than on the continent.

| Indicator | UK's position |

|---|---|

Affordability of space heating | 16/16 |

Arrears on utility bills in last 12 months | 14/16 |

Level of fuel poverty | 14/16 |

Homes in poor state of repair | 12/16 |

Thermal performance of walls | 7/11 |

Thermal performance of roof | 8/11 |

Thermal performance of floor | 10/11 |

Thermal performance of windows | 11/11 |

More efficient buildings have lower energy demand, making heat decarbonisation easier.

European countries making progress on heat like France and Denmark have rolled out programmes to improve the energy efficiency of their buildings, including schemes that offer tax credits for improvements (France), or minimum requirements when renovating a property (Denmark).

Belgium and Germany are taking the idea of Energy Performance Certificates a step further with the introduction of Building Renovation Passports. These provide the owner with personalised suggestions on specific actions they can take on their buildings over an extended period of time. The process includes an onsite audit and developing a series of indicators, which are based both on the occupant’s needs and the age, financial situation and composition of the household.

For example, Germany’s energy ministry adopted “individual renovation roadmaps” in 2017. It includes customised measures which link into national building performance targets and aims to put the building owner at the centre of the process. France and Flanders in Belgium are also testing the concept.

Moving away from gas in the Netherlands

The UK is unusually reliant on natural gas as a source of heat. The situation in the Netherlands is similar, with around 95% of homes heated by gas.

But the country has been deemed a trailblazer with plans to phase out unabated natural gas consumption and production by 2050. This was prompted by public concern over damage from induced earthquakes at its Groningen gas field, a reliance on Russian gas imports and climate change.

A phase out date for gas heating installation in new homes has been set as 2021, although exemptions will be possible. A 2017 coalition agreement plan targets making 30,000-50,000 existing houses “natural gas free” as a first step. The Netherlands has a target to switch 1.5 million homes from natural gas by 2030 – although it is not currently on track to meet this – with all 7.7 million Dutch homes ‘sustainable’ by 2050.

The Netherlands’ Climate Accord, finalised in June 2019 by industry, trade unions, NGO and local authorities, targeted buildings as one of its five focus sectors. A key component is placing taxes on natural gas use to discourage consumption, with levies increasing from 2020. This additional tax take will be used to reduce electricity costs, leaving household bills largely unchanged.

Local authorities will be tasked with developing “regional energy strategies”, to allow stakeholders such as housing developers and citizen groups to feed into the plan for their area. This regional approach stands in contrast with the UK’s more top down, national policy approach thus far on heat.

Around half of the Netherland’s new heating systems are expected to be district heating networks, which will be fuelled by industrial waste heat, geothermal energy, solar, biomass, power to heat or biogas.

A further quarter are expected to be electric heat pumps and the remaining quarter electric/gas-fired hybrid heat pumps part powered by “green” gases such as biogas and biomethane.

Heat pumps

Heat pumps use is much more widespread in other countries, especially in Scandinavia. Currently around 90% of European sales are air source heat pumps, with just one in ten extracting heat from the ground.

Many of the EU countries which have achieved high heat pump sales are those without large-scale natural gas production. Countries like Sweden and Switzerland have lots of hydro power which can provide lots of low carbon electricity for their heat pumps, for example, and their electricity grids are reinforced for this high demand. In 2018, France too had a high proportion of renewable energy from hydroelectricity (12%) and wind (4%).

Long-term policy stability and financial support for heat pumps has also boosted take up. In Austria up to 30% of the cost of air source heat pumps (< 400kwh) is subsidised plus an additional €35 - 70 per kW of thermal energy delivered to the household.

Putting standards in place for manufacturing, installation and maintenance of heat pumps is important in order to establish industry’s reputation. Germany makes a good example of this: poor installations, a lack of maintenance and low installer experience are thought to be part of the reason the heat pump market crashed in the mid 1980s. The market recovered once effective quality control measures were put in place and there are now a total of 880,000 heat pumps in Germany – new installations in 2018 alone were 40% higher than in 2012.

Heat networks

Most large-scale heat network developments have a strong element of planning policy. Denmark, where heat networks reach 63% of the population, made it mandatory to connect heat or natural gas networks where they are available, even banning heat pumps in collective supply areas. It then subsidised heat pumps outside areas of collective supply.

The majority of suppliers in Denmark are also municipally owned or cooperatives: private operators have been discouraged since no suppliers are allowed to charge customers more than the cost of providing heat.

The country expects at least 90% of district heating consumption will come from clean energy sources by 2030. It is also planning several interconnectors with other North Seas Countries to boost security of supply as the share of wind and solar power increases and construction started on such a subsea cable between the UK and Denmark in July 2020.

Germany and Italy, who both use high amounts of natural gas, also have an explicit focus on replacing gas grids with heat networks. It’s thought that 2.7 million homes in Germany could be easily linked into a district heating pipeline and in Italy the district heating sector is growing; it served 3.9 million citizens in 2019 with potential to cover a quarter of all heat demand in future.

Scotland, although a part of the UK and therefore with some policy levers surrounding heat centralised to Westminster, are also making moves in renewable heating. Over the course of the next Parliament, they have committed to increasing heating retrofits, from just 2,000 installations per year in 2020 to 64,000 homes fitted in 2025 – a cumulative total of around 126,000 homes. That’s 5% of Scotland’s housing stock in one policy alone, likely to be mainly heat pumps and heat networks.

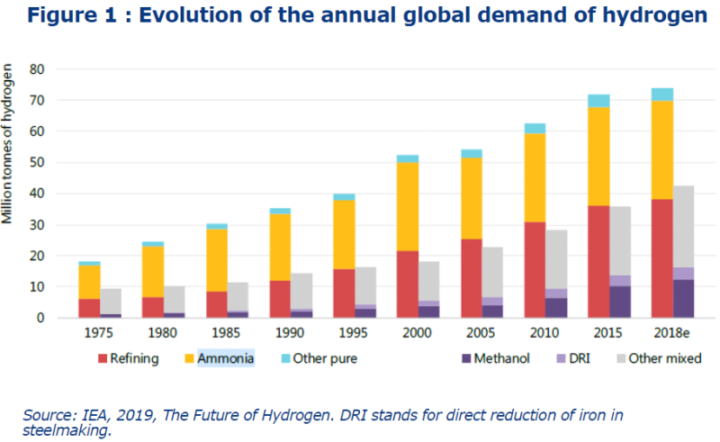

Hydrogen

The EU recently revealed plans to develop the hydrogen economy for hard to treat sectors like chemicals and steel, as well as being a long term solution to some transport needs like shipping and aviation. There’s more on how hydrogen can be used for heating in this ECIU briefing.

Their strategy indicates that by 2050, clean hydrogen could meet 24% of global energy demand, generating €630 billion in sales. For Europe, that could translate into 1 million jobs in the hydrogen value chain. However, renewable hydrogen has still not been fully developed at scale – 96% comes from fossil fuels like gas – so the EU Commission has recognised that ‘the priority is to develop renewable hydrogen, produced using mainly wind and solar energy’.

France, Germany and South Korea all have aspirations to scale up hydrogen technology, with France investing €90 million, Germany €9 billion solely on hydrogen from renewable sources, and South Korea even more at €19 billion to establish a public-private hydrogen vehicle industry by 2022.

There is much to be done to decarbonise heating in countries across Europe and further abroad. The best way forward, and the differing routes played out by different regions, will be crucial when attempting to meet respective climate change targets.